The June and July consumer media headlines reflected the ongoing pressure on restaurants. Tight finances and mounting job market pressure have led to lower consumer confidence and more trips to the grocery store. Consumers are making more home-prepared meals across all occasions, but also integrate grocery deli-prepared foods and meals more often as they balance money against time, nutrition, mood, sustainability and more.

- In addition to the widely reported bankruptcy filings by Red Lobster, Buca di Beppo, Rubio’s, World of Beer and several small restaurant chains filed for Chapter 11 bankruptcy in the past few months. Other restaurant chains, including TGI Friday’s, Hooters and Arby’s closed multiple underperforming locations. In response to consumers’ financial woes, many restaurants are turning to value, such as McDonald’s $5 meal deal.

- For restaurants and grocery stores alike, the changes are predominantly driven by lower-income consumers. According to the Circana survey, 63% of households with annual incomes of up to $25,000 bought restaurant food at least once in June compared to 85% of households making at least $100,000.

- Restaurant price increases continued to outpace food-at-home inflation, at +4.1% versus +1.1%, according to the June Bureau of Labor Statistics (the latest available at the time of publication).

- Lower-income households were also more likely to implement money-saving measures when shopping for groceries, at 84% versus 76% of upper-income households. Lower-income households especially over index for buying less and sticking to the budget, switching to store brands and shopping at value retailers. All income levels and ages are focused on sales promotions and coupons.

- A new report by the U.S. Department of Agriculture predicts that food prices will continue to decelerate. Prices for all food are now predicted to increase 2.2% over 2024, with food-at-home prices projected to go up just 1.0%. The 2025 forecast expects a 2.0% price increase for total food, with a below-average anticipated increase of 0.7% for food-at-home prices.

Inflation insights

In July 2024 (the four weeks ending 7/28/2024), the price per unit across all foods and beverages in the Circana MULO+ universe stood at $4.22, an increase of 1.5% versus July 2023. This is also a slight uptick from the 1.3% price increase seen in June. Prices in the fresh perimeter were up 2.3% year-over-year in July. This marks the first time in quite a while that fresh item inflation was higher than that in the center of the store that averaged an increase of 0.9% year-on-year. The average price of $4.22 is 34.8% higher than the 2019, pre-pandemic average of $3.13.

The average price per pound in the meat department across all cuts and kinds, both fixed and random weight, stood at $4.71 in July 2024, up 2.3% from year-on-year. The average processed meat price stayed above $5, up 1.4% versus prior-year levels.

July brought a mix of price movements. Pork, beef and bacon, in particular, experienced increases in price. This is a reversal for bacon that had been experiencing deflation throughout much of 2023 and the early part of 2024. Lamb, turkey, packaged lunchmeat, smoked ham and processed chicken experienced substantial price declines.

July brought a mix of price movements. Pork, beef and bacon, in particular, experienced increases in price. This is a reversal for bacon that had been experiencing deflation throughout much of 2023 and the early part of 2024. Lamb, turkey, packaged lunchmeat, smoked ham and processed chicken experienced substantial price declines.

Meat sales

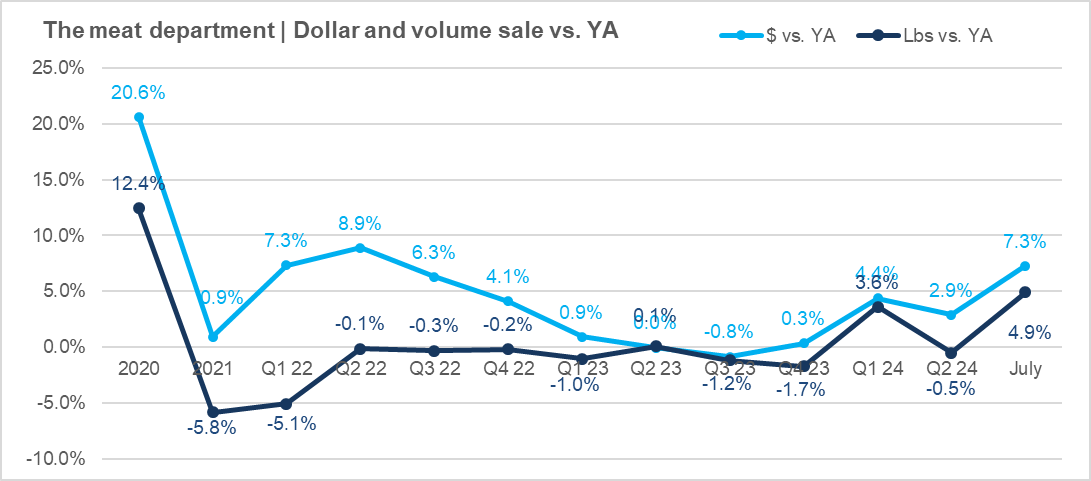

July was a very strong month for the meat department, especially on the fresh meat side. The four July weeks generated $8.1 billion, which was up 7.3% over July 2023, with pound gains of 4.9%. Circana time periods end on a Sunday, which moved the majority of this year’s July Fourth sales into the month of July due to the Thursday timing of the holiday. Last year, holiday sales were split between June and July.

In the 52-week view, dollars now trend 2.7% ahead of last year. This increase reflects a combination of mild price increases and strong everyday and holiday demand for meat and poultry as the world has turned home-centric once more.

All July weeks experienced volume growth in comparison to year-ago levels. The first week, reflecting the holiday sales, generated $2.3 billion in meat and poultry sales, up 14.4% in dollars and 12.2% in pounds. Yet, the strong holiday week results did not impact everyday demand in the weeks to follow.

With July delivering another strong performance, the year-to-date meat department sales reached $58.7 billion, which reflects an increase of 4.0%. Year-to-date pound sales reached 12.6 billion, which is up 1.8% over the same period last year.

Assortment

Meat department assortment, measured in the number of weekly items per store, averaged 424 SKUs in July 2024 — holding steady around 50 items below pre-pandemic levels.

Fresh meat sales by protein

The big grilling holiday brought home the win for beef that generated $3.1 billion in July and $38.3 billion in the 52-week period. Beef pound sales increased 7.9% over July 2023, pulling the 52-week total up to +1.5%. Chicken, the second-largest seller in dollars, also had a strong month and year, with consumers benefitting from chicken’s favorable price per pound. Lamb’s deflation translated into more pounds sold, with a robust increase of 15.3% in July.

Processed meat

Processed meat also had a strong July performance. Dollar sales increased 4.0% over July 2023 and pound sales grew by 2.5%. Reflecting the holiday’s impact, frankfurters and dinner sausage led the volume gains. Bacon, experiencing growing inflation once more, was the only processed meat to experience a decrease in pound sales.

Grinds

Ground beef had a monster month, with $1.2 billion in sales during the four July weeks. This was an increase of 8.1% in dollars and 5.2% in pounds. Turkey and chicken had a strong month as well. The ground lamb performance was far below its total year levels, which could be due to it being leveraged as an in and out item for some grocery chains, in which case the timing of a promotion can prompt substantial swings in the shorter four-week periods.

What’s next?

- The summer season is coming to an end with the back-to-school season in full swing for a number of the Southern states. This may change sales patterns for lunchbox-type items.

- Labor Day, which will be observed on Monday, Sept. 2, will mark the unofficial end of grilling season, though weather patterns in the early fall tend to have a substantial impact on sales as well.

- All consumer confidence, restaurant and grocery indicators point to a more home-centric environment for the time being, compounded by ongoing higher restaurant inflation and a cooling job market.

Date ranges:

2023: 52 weeks ending 12/31/2023

Q1 2024: 13 weeks ending 3/31/ 2024

Q2 2024: 13 weeks ending 6/30/2024

July 2024: 4 weeks ending 7/28/2024