May 2024 provided the first clean year-on-year performance look, with March and April affected by the earlier Easter timing that moved the substantial holiday sales from the second to the first quarter of the year.

- Consumer sentiment, that took a big dip in April, declined further in May. The University of Michigan expectations index fell to 68.8 in May 2024, down from 76.0 the prior month. Consumers expressed concern over labor — expecting unemployment rates to rise and income growth to slow. Meanwhile, consumers remain worried over the lingering and cumulative impact of inflation.

- Food-away-from-home (restaurant) prices increased 4.0% year-over-year in May versus 1.0% for food-at-home, according to the Bureau of Labor Statistics.

- The first five months of the year show a slowdown in restaurant traffic echoed by 27% of consumers in Circana’s May survey of primary grocery shoppers who say they are eating at restaurants less often. Where 80% of respondents consumed restaurant food in May, only 70% of lower-income households did so versus 87% of upper-income households.

- Lower-income households are also more likely to implement money-saving measures when shopping for groceries, at 87% versus 73% of upper-income households. Lower-income households are far more likely to buy less/stick to the budget, switch to store brands and shop at value retailers. All income levels and ages are focused on sales promotions and coupons.

Inflation insights

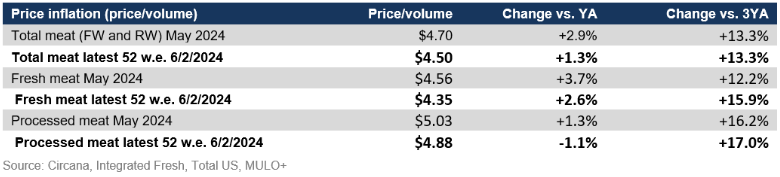

In May 2024 (the five weeks ending 6/2/2024), the price per unit across all foods and beverages in the Circana MULO+ universe increased 1.2% versus May 2023. Prices in the fresh perimeter were up 1.2% in May versus year ago, whereas center-store grocery prices increased 1.7% — the closest rates of inflation seen in several years between the two parts of the store. The May prices across food and beverages were 33% higher than they were pre-pandemic.

The average price per pound in the meat department across all cuts and kinds, both fixed and random weight, stood at $4.70 in May 2024, up 2.9% from year-on-year. The average processed meat price moved above $5, up 1.3% versus prior-year levels. May inflation exceeds the 52-week inflation levels for both fresh and processed meat.

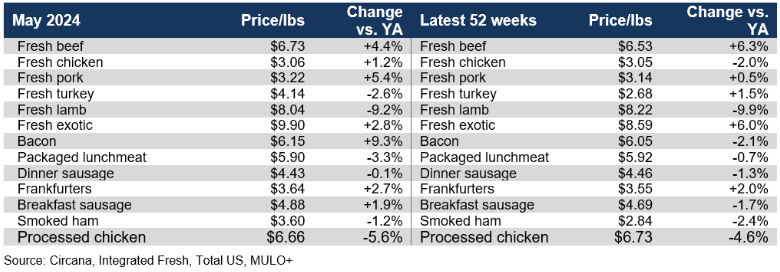

May brought a mix of price movements. Pork, beef and bacon, in particular, experienced increases in price. This is a reversal for bacon that had been experiencing deflation throughout much of 2023 and the early part of 2024. Lamb, turkey and processed chicken experienced substantial price declines.

Meat sales

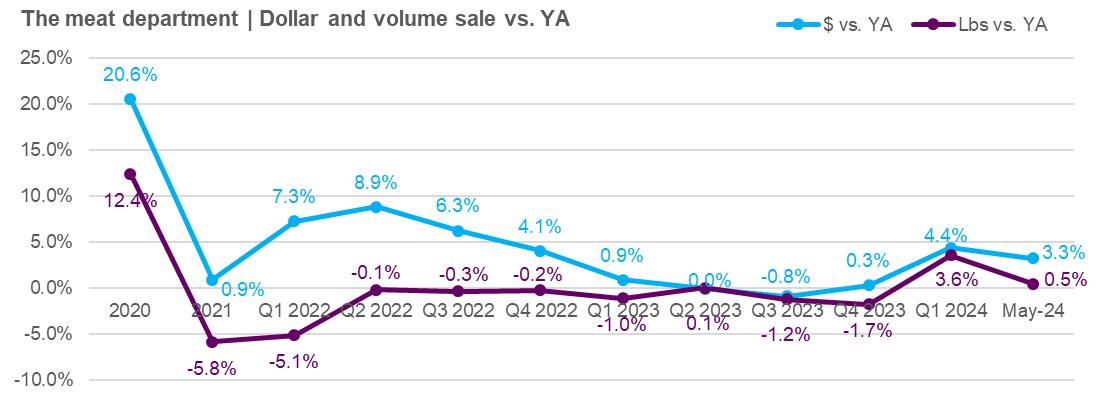

Year-to-date, volume sales have been positive every month with the one exception of April when the shift in Easter timing overrode the general strength of everyday demand. In May, fresh meat pounds were up 1.5% versus last year and 2.5% versus two years ago. This more than offset the declines in processed meat, resulting in a 0.5% pound increase for the total meat department.

In the 52-week view, pound sales also pulled into positive territory, up 0.6% versus last year and up 0.2% versus two years ago. This is also driven by the strength of demand for fresh meat.

Four out of the five May weeks experienced volume growth in comparison to year-ago levels. The final week ending June 2 pulled down the positive momentum to result in the 0.5% increase for the entire month of May.

With May delivering another strong performance, the year-to-date meat department sales reached $42.6 billion, which reflects an increase of 3.7%. Year-to-date pound sales reached 9.3 billion, which is up 1.8% over the same period last year.

Assortment

Assortment

Meat department assortment, measured in the number of weekly items per store, averaged 429 SKUs in May 2024 — holding steady around 40 to 50 items below pre-pandemic levels.

Fresh meat sales by protein

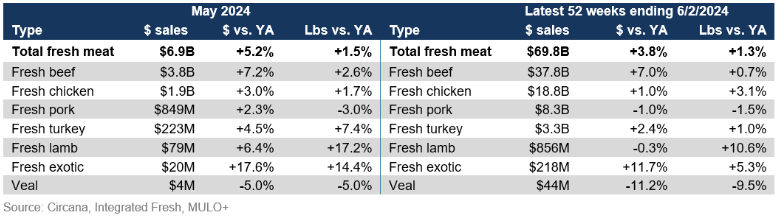

Fresh meat sales continued to strengthen in May, with pound gains for all but pork and veal. In the 52-week view, more and more proteins are starting to track ahead year-on-year in pound sales as well. This includes fresh beef that has experienced above-average inflation due to tight supply conditions. Fresh chicken increased pound sales 3.1% year-on-year and lamb (while a smaller seller) is pacing 10.6% ahead of year-ago levels.

Processed meat

Processed meat overall experienced declines in both dollars and pounds in May, however, some items continued to do well, including dinner and breakfast sausage, smoked ham and processed chicken. In the full-year view, pounds are tracking 1% behind year-ago levels, with an above-average performance for bacon, dinner and breakfast sausage.

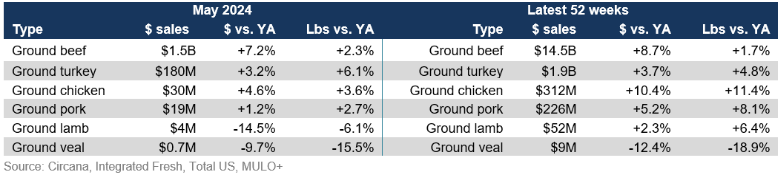

Grinds

In addition to the strong performance by chicken in the current environment, grinds did well also. Ground beef, despite the inflation seen in the beef category, increased pound sales by 2.3% in May. In the full year view, beef pounds increased 1.7%. Ground chicken and pork also had strong performances.

What’s next?

Looking forward to the many summer holidays and happenings:

- 17% of consumers in the May Circana survey plan to travel more than last summer whereas 10% will travel less often or take smaller trips. Eight percent are not planning on traveling at all while they did so last summer. Plans are impacted by the price of travel (34%) or the lack of money for travel because price increases on everyday needs (47%). For food retailers, staycations provide an opportunity to create special moments at home.

- 65% plan to do a cookout or barbecue this summer.

- 63% plan to host friends and family.

The next performance report in the Circana, 210 Analytics and Hillphoenix series will be released mid-July 2024 to cover the June sales trends.

Date ranges:

2023: 52 weeks ending 12/31/2023

Q1 2024: 13 weeks ending 3/31/2024

May 2024: 5 weeks ending 6/2/2024