State of the Industry 2023: Overview

Post-COVID hangover lingers

Ongoing labor challenges power embrace of automation.

Opening video credit: GettyImages / Floaria Bicher / Creatas Video+ / Getty Images Plus / Getty Images Plus

Other images courtesy of Hudson Riehle, senior vice president of research at the National Restaurant Association

State of the Industry Articles:

The U.S. and the world are suffering through the post-COVID hangover, trends that were beginning prior to the outbreak but kicked into hyperdrive. Now we are trying to figure out what is normal. Inflation is rampant, and our supply chain is just normalizing. During COVID, younger consumer segments learned how to cook rudimentary dishes. Most groceries and restaurants offered delivery. People liked changes, now they may be permanent. People have turned into germaphobes and are continuing to social distance. This has impacted sit-down restaurants and filled up drive-through lines. Consumers are shopping less frequently and buying more when they go. Economists thought that the 2022 trends would continue into 2023. This has resulted in an excess supply of protein, dairy, and other products. Consumers continue to explore fad diets and bold flavors. Different segments have reacted differently.

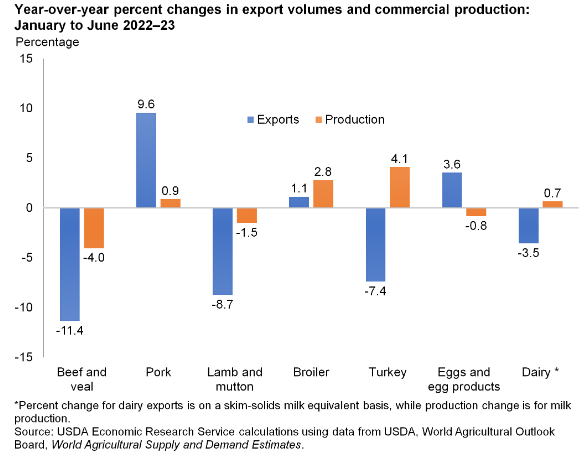

The beef industry is now experiencing a shortage of cows because of farmers thinning their herds during the drought of 2022. This is what happened in 2012. When grasslands are unavailable, and hay is expensive farmers thin their hurds. Turkey supply dramatically impacted by bird flu force the depopulation of a large number of birds, also impacting egg producers. This droves favorable prices for producers that had product and negatively impacted the earnings of those who did not have product. The pork industry is oversupplied because exports make up a sizable portion of their demand, China is no longer suffering from African swine fever, reducing demand for exports.

Chicken producers anticipated a similar year to 2022, including additional growth in supply, creating a surplus. Because poultry producers can adjust supply quicker than other proteins, they are now reducing flocks returning supply into balance. These external factors always impact other proteins, which create market share for those proteins with extra product.

As of July 31, the total frozen poultry supplies were up 4% from July 31, 2022. Beef stocks are down by 18% for that time period. Pork bellies increased 21% from the same period last year. Frozen pork supplies decreased by 10% from the previous year.

The conflict in Ukraine continues to drag on, and it is affecting certain commodities and impacting supply chain. This will continue for at least the next 12 months. As a result of this and other international factors, we are seeing the world economy start to shift from a global focus to a regional one.

Labor outlook

Staffing is a huge problem in all categories. The retail workforce is the No. 1 concern of most grocery CEOs, expressed at FMI’s Midwinter Executive Conference in 2022. Dana Peterson EVP and chief economist for The Conference Board, told the food industry gathering, “Our belief is that labor shortages are here to stay.” There are a multitude of reasons: the pandemic, poor wages, retiring baby boomers and immigrant labor issues and more. They face a pool of workers who do not want to work in retail. There is also a shortage of truck drivers, poultry/meat processing workers, and supermarket and restaurant workers. AI and automation will be important in all categories to replace menial activity with machines that come to work every day performing any practices that are predictable.

Grocery trends

Consumers are enjoying their newfound ability to cook by using the Internet to research new recipes and ideas. Retailers and restaurant operators have shortened their assortment, giving consumers fewer choices. It has impacted certain categories and benefited others. Post-pandemic, home delivery and curbside pickup are an expected part of the foodservice experience. Retailers struggle to pass on related costs. For example: A Giant grocers’ fulfillment center opened months ago is now set to close, along with two other complexes, reports local Washington D.C. news group WTOP. The fulfillment center, which opened in May in Manassas, Va., opened with the goal of completing delivery orders in just three hours. Now, Giant is changing its operating structure and wants to use a localized, more efficient fulfillment model. The other centers set to close are in Hannover, Md., and Milford, Del. This is a similar approach to those taken by Walmart, Target, and other national and regional retailers. *

Empowered consumers who aspire to healthful habits are fueling the rise of clean labels, making information transparency mandatory. As new diets continue to gain traction, Nestle and other food marketers are using AI to analyze trends, ingredients, flavors and health benefits from social media, online publications, and other web sources to discover contemporary trends for product ideas.

Retail consolidation continues. The Kroger-Albertsons deal, if it goes through, will have a significant impact on the grocery landscape. There will be about 1,000 stores that will be divested to other owners, Aldi is buying Winn-Dixie. Publix and Meijer continue to expand. Big box stores, limited assortment/dollar stores and club stores continue taking market share from traditional supermarkets. Consumers are much more conscious of germs, food safety, sustainability, and other issues.

Inflation affects

Consumers’ wages in general have not increased enough to keep up inflation, lowering their spending power. They are adjusting their spending habits to survive. Inflation also plays a pronounced role in declining sales of plant-based meats. As a result of Inflation, older consumer segments are trading down to private-label brands to compensate. Youngers consumers cut back in some areas but are often willing to splurge on some items like indulgent foods.

Gen Z consumers are becoming trendsetters, and going forward this trend will escalate. Gen Z are the 68.6 million consumers born between 1997 and 2013. By 2025 Gen Z will make up 27% of the workforce. * This consumer group is more informed, more suspicious and their frequency of change is high. Build your business to be flexible because things will change rapidly, and you will have to adapt to the whims of this group. We must understand all shoppers from all generations to be successful. Gen Z has been influenced by the digital age, climate anxiety, COVID, global unrest and financial insecurity. Gen Z has the least-positive outlook and the highest percentage of mental illness of any generation. Unpaid student loans and of course the educational disruptions due to COVID have contributed to their anxiety. 62% like the appeal of “indulgent” recipes — also for being simple to make (61%) and perceived taste (59%). However, 41% of those who prefer indulgent recipes like its inherent trendiness and share on Instagram. Sixty-nine percent find themselves “liking” and “favoriting” healthy recipes they spot on social media. By comparison, 63% like and favor the indulgent recipes they see online. Even when it comes to their own recipes, 73% admitted they spend extra time preparing their meals just to make them more picturesque for social media. When trying out a new recipe, 46% of respondents enjoyed the meal for themselves, but also shared the meal with their family (25%) or friends (10%) ... *

Restaurant trends

Consumers have returned to the restaurant. Dollar sales are back to 2019 levels, but purchase habits and behaviors have changed. The drive-throughs are full of cars. Sit-down dining has declined from pre-pandemic levels. Venture capital is now a major player in restaurant ownership. They came on board at the very worst time before the pandemic hit. The restaurant ownership is carrying a huge burden of debt. An Exodus in staffing occurred during the pandemic. Many of these workers found other opportunities, they liked the change, and they are not coming back.

By the end of 2021, dine-in visits to fast food chains had fallen to just 14% of restaurant traffic, compared to 28% pre-pandemic, according to the NPD Group. Consumers are scarfing down their burgers and fries at homes, at their offices, in their cars and anywhere but in the restaurant.

Compact stores that harness automation and digitalization require diners to order with mobile apps or digital kiosks delivering orders in record time. Chains are shrinking their dining rooms, to match drive-through demand increases and digital ordering. Burger King, KFC, Wingstop, IHOP and others are experimenting with pre-packaged food is to go, and limited seating. Robotic fry cooking will automate the fast-food experience to be faster and cut labor.

Convenience drivers have become more important. Even before the pandemic, about 61% of fast-food sales were off premises. Reaching a high of 90% during lockdowns, they are now hovering around 75%. Fast food restaurants have become a pit stop and less of a place to eat and hang out. Now a transitory space to pick up or hand off food. Chains can dramatically cut one of the industry’s operating costs: paying human employees.

Sources

* Originally published on Forbes.com FMI’s Midwinter Executive Conference in 2022

Picture courtesy of Hudson Riehle, senior vice president of research at the National Restaurant Association

Charts published by the USDA and meat Data published August 2023

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!