2016 Consumer Trends Report: Searching for a story

Meat and poultry still play an important role in the American diet, but more consumers — particularly those in the younger generations — want the facts behind the meat they eat.

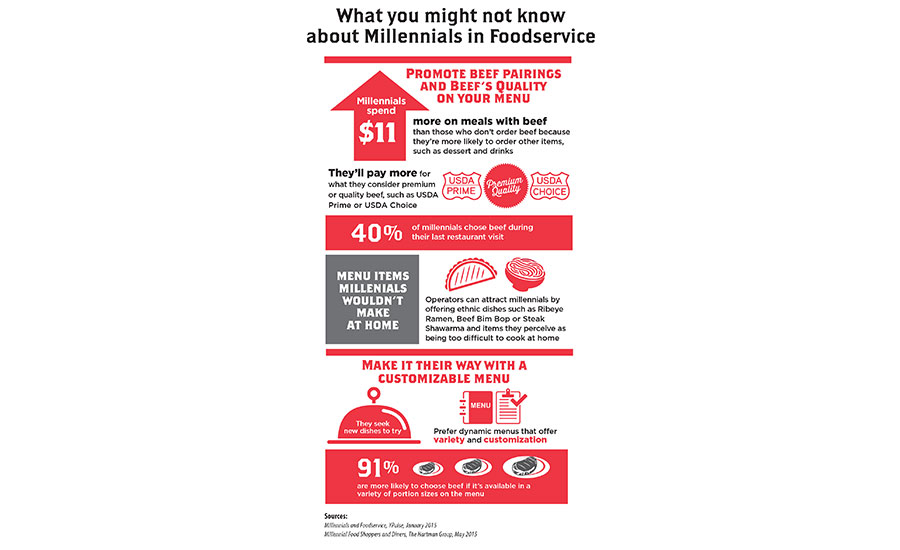

Millennials are willing to pay more for what they consider premium or quality beef, are attracted to dishes they consider too difficult to cook at home, and prefer a dynamic, customizable menu.

Primary shoppers are the most common at 43%, while secondary shoppers make up only 10% of types of grocery shoppers.

The simple act of buying food at a restaurant or a grocery store has never been more challenging, thanks to an overload of online data, news reports and opinions widely available to every consumer. The saturation of information and misinformation has made it difficult to tell fact from fiction, or science from nonsense.

As a result, tracking consumer purchasing information is no longer a matter of seeing which protein happens to be the most popular or the best value at the moment. When discussing consumer trends, it’s impossible to leave out all the mitigating factors that affect consumer preferences. Confusion about GMOs, arguments about antibiotics, concerns about animal welfare and other issues have made more shoppers look for products that ease their conscience as well as fill their bellies. When buying a pack of chicken breasts, consumers more than ever need to know just how and where that chicken was raised, what it ate, what medicines it took and how it died.

If one thing is certain, it is that the future of the meat industry is still in good hands as the Millennial generation comes into its own. While they might not include protein in every meal, Millennial shoppers are heavy consumers of beef, pork, poultry and other meats. Although their needs and preferences may set them apart from past generations, they will still look to the meat industry to fill their plates with healthy food for themselves and their families.

“Millennials spend more proportionally on fresh red meat than any other generation and were the only group in our study to indicate that they planned to spend more on red meat next year than they did this year,” says Brian Bell, vice president, Cargill Beef North American Sales and Marketing. Cargill recently initiated a proprietary red meat consumer study of more than 8,000 fresh meat consumers to better understand attitudes, needs and behaviors. “The key to keeping these consumers engaged is understanding their needs at the meat case.”

A look at the numbers

According to the most recent Mintel surveys of packaged red meats and poultry products, beef reached sales of about $35.2 billion in 2014 and is expected to remain relatively flat through 2019.

“Since beef supplies are predicted to remain tight for some time, consumers will continue to turn to less-expensive protein sources, such as poultry and vegetarian items,” the company reported.

Sales of pork products reached $10.8 billion in 2014 and are also forecasted to decrease or remain flat, reaching $10.9 billion in 2019. Sales of other red meats, including lamb, goat and game meats, are projected to increase from $1.3 billion in 2014 to $1.5 billion in 2019. Category growth is being spurred by Millennials, who are comfortable eating a variety of meats, due to this population’s multicultural makeup.

The poultry market, which grew 16 percent from 2009 to 2014, reaching $24.1 billion in sales, is forecasted to grow an additional 21 percent through 2019. Although chicken is the dominant bird, sales of turkey, duck and other birds grew faster due to increased interest in other poultry, with consumers looking for alternatives to red meat and greater availability.

At the foodservice level, consumers are continuing to visit fast-casual restaurants at the expense of quick-service restaurants (QSRs). According to Mintel, there was a 5 percent decrease in the number of consumers visiting a burger or chicken QSR within the last month, from August 2014 to August 2015.

Mary Chapman, senior director, Product Innovation, for Technomic Inc., says that consumers, particularly younger ones, are eating more vegetarian options or seafood, due in part to the higher prices for proteins.

“Our research has found that almost half of consumers have noticed that beef prices are up at restaurants,” she adds. “About one in five say they’re purchasing lower-quality/’value’ cuts as a result, and a similar share says they are ordering non-beef dishes instead.”

Along with the move toward better-quality burgers and chicken, maintaining a healthy diet is also affecting where people go to eat. One-third of consumers surveyed by Mintel report that they are ordering healthy items more often this year compared to last year. Parents, particularly fathers, are leading that movement.

“Burger and chicken restaurants may find the perception of offering unhealthy foods an obstacle in a market where consumers say they want better-for-you (BFY) foods,” Mintel reports.

Consumers are also looking at more exotic proteins, from lamb, goat and bison in the red meat side to duck and quail on the poultry side. Technomic’s Beef & Pork report noted that 13 percent of those surveyed reported eating more game meat than a year ago. That figure certainly includes some people who tried it once, didn’t like the taste and won’t purchase it again. Still, shoppers are feeling more adventurous, and as Chapman notes, “Adventurous diners are more likely to order these proteins at a restaurant or purchase them at a store.”

Another niche that has grown in popularity is meats with desirable attributes — organic, natural, free-range, antibiotic-free, GMO-free. Cargill’s survey found that nearly 70 percent of consumers are interested in red meat that comes from certified humanely raised and handled animals on farms that are routinely audited.

That interest holds true for the foodservice sector as well. Mintel states that nearly 70 percent of fast-casual customers said they would pay extra for premium toppings. Even at the QSR level, more than half of those surveyed would pay more for premium ingredients, indicating that there is a market for premium items throughout the foodservice sector, provided that the restaurants can prove to their customers that their ingredients are indeed premium.

Consumers also gravitate to those words on meat labels in supermarkets. However, those attributes come at a price, and not everyone is able to afford them. Furthermore, the public may not be clear as to the definition of those terms. Chapman notes that a number of consumers think that things like natural, GMO-free, organic and locally raised make meat taste better and more healthful. While a shopper may be able to detect the difference between a grain-fed and a grass-fed steak, for example, it would be difficult, if not impossible, to tell the difference between a GMO-free pork chop and a commodity equivalent.

Bell says that Cargill has worked to prioritize which claims are most relevant and meaningful to consumers.

“We’re making strides to help meet these demands but also recognize the importance of educating consumers so they understand what these claims truly mean,” he adds.

Those and other types of attributes help determine quality for many consumers. “Quality” is a nebulous term and can mean different things for different consumers. The definition can also change depending on the generation of the shopper.

“For Millennial and Gen X consumers, quality means emphasizing the story of their food — where, how and by whom it is produced,” Bell explains. “More transparency about how animals are raised, and by whom, is critical to their purchase decisions.”

Baby Boomers, on the other hand, tend to view quality of red meats in more traditional terms: marbling, grade, juiciness, tenderness. They are willing to pay more for those premium claims. Others in the Boomer generation see meat as a more commodity item; they will expect a safe, quality product but are not willing to pay a premium for it. Taken as a whole, the Baby Boomers are the most loyal customers to the meat industry.

“On the other hand, Gen Xers view quality not only as the tenderness of the product but also as their ability to discern where, how and by whom their food was produced; quality to them truly means transparency of how their food was raised,” Bell adds. “And last, much like the Gen Xers, Millennials care about food with a story, but are not always willing to pay for these claims.”

Those youngest consumers are still building up their household incomes and figuring out their routines. Additionally, they are not comfortable with preparing red meat yet, so “quality” to them can also mean an easy, fool-proof meal option.

When it comes to the types of red meat products they buy, the Baby Boomer, Generation X and Millennial generations all have their own needs and preferences. Bell says that the quality-conscious Boomers have a passion for food and know which cuts to buy and how to prepare them.

“[They] mainly purchase red meat to connect with others through a special occasion or a chance to share a nice meal with friends and family; they are most often looking to purchase beef tenderloin, Ribeye steak and Porterhouse steak,” he says.

The more value-conscious Baby Boomers purchase red meat as part of their usual routine meals, although they are among the most likely to reward themselves by indulging in a more extravagant meal. When they do indulge, they choose a steak almost a third of the time.

A large number of Generation X falls into the “foodie” category, so they seek out products with claims and stories that they can share with friends to help bolster their reputations, Bell says. Their favorite red meat products include steak, brisket and pre-marinated meat. Millennials share some of those same motivations, though they might not be able to match the Gen X behaviors due to differences in life stage and incomes. They have a busy lifestyle and need information about preparing food, complementing cuts and latest trends.

Mintel reports that the desire for transparency about where and how poultry is raised will continue to be an important issue for poultry brands. More than two-thirds of people surveyed (68 percent) are interested in knowing where their poultry comes from, and 62 percent are interested in knowing how their poultry was raised. Brands that can educate consumers about product origin and how their poultry is raised, as well as ways to properly handle poultry, will have an advantage. Additionally, they will be able to build that sense of trust that is so important and influential on poultry purchases.

The net result is that transparency is key for consumers of all ages. Consumers are demanding more from their food manufacturers than ever before, and companies have to adapt to those demands in order to remain relevant.

“We clearly label our products so consumers know exactly what they are getting, whether it’s a USDA Prime Porterhouse Steak or a more affordable, all-real beef option like ground beef with finely textured beef, we want them to feel confident and comfortable with their purchase decisions at the meat case,” Bell says.

A trend worth noting is the emergence of food as a craft, and not a commodity. Outside of the meat category, it can be seen with the growth of craft beers, farm-to-table restaurants and farmers’ markets. Within the meat industry, it can be observed by the increased recognition of the butcher as a craftsperson. More and more courses are giving consumers the opportunity to learn the art of butchery, so they can better understand the various chop and steak cuts.

Elsewhere, companies are experimenting with gourmet sausage flavors, locally raised meats, and species-specific beef, pork and poultry items. Small processors in particular have grown tremendously by creating craft meat items, and it’s a trend that has caught the eye of even the largest companies.

“We’re already seeing this [trend] come alive with craft burgers, and it makes sense. Our research shows that consumers are seeking adventure in food and gravitating toward regional flavors — two elements often found in craft brands,” Bell says. “At Cargill, nothing is off the table. We’re studying food trends and how they align with consumer demand to constantly evaluate our product offerings and determine what the best product mix looks like for our retailers and their consumers.”

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!