The Crop Report 2024

Abundant 2024 crop and higher carryover from 2023 push feed costs lower

Increased presence of crop imports heightens competition.

Photo Credit: Minnesota Corn Growers Association

This is the 14th year our crop report featured in The National Provisioner. Every year is vastly different, with a separate set of global circumstances. The reason crops are important is that feed ingredients represent approximately 50% of our overall cost. Because prices fluctuate so dramatically, it is a very unpredictable component of our business. What is different from other years is that carryover of corn, wheat and soybeans has recovered significantly from 2023. Acres planted are nearer record high, and crop conditions remain better than last year.

We still have a war in Ukraine. Ukraine and Russia make up 47% of the global potash supply. Ukraine has rich soil and has been a major exporter of wheat to countries that cannot produce enough. Because of the war, both have been disrupted. One of the other major sources of potash is in Canada and fortunately they have been making up some of the deficit left by Ukraine and Russia.

Because Russia has historically been a major importer of leg quarters, this part of the bird has also been disrupted. With the leg quarters being more than 50% of the bird’s weight, when its price is disrupted by war or politics profitability is dramatically lower. US consumers looking for value have discovered leg quarters. The crop conditions in Brazil are also a factor. For the first time Brazil, now a major corn and soybean producer, exported a significant amount of soybean crush into the Eastern US, changing the balance of supply.

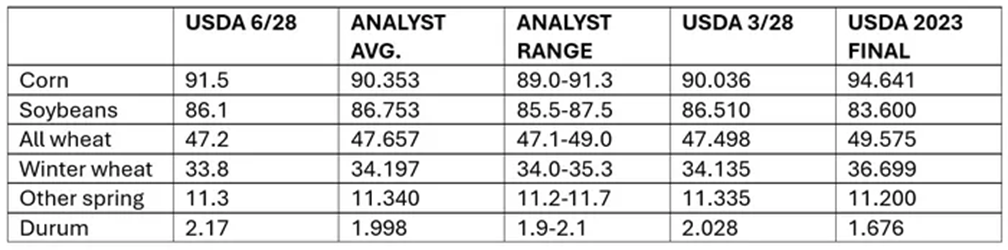

U.S. plantings of major crops for 2024 harvest (in millions of acres)

This year the weather has been cooperative, and acreage is near a record high. As this is written in early July, rain is critical in the next 45 days, if for some reason it does not rain, like it did in 2011, that can also dramatically impact crop yield and prices. Another key factor is the carryover of corn and soybeans from 2023. This year carry has dramatically increased compared to 2023. All these factors will push prices lower on corn, soybean and wheat. In the US, our primary feed component is corn/soybean crush whereas in the EU wheat is used as a substitute for corn, it is not as efficient at converting feed to meat.

Crop carryover from 2023 harvest Source: USDA 6/28

Key findings released in the USDA Acreage report include June 28.2024:

- The planted acreage report showed farmers have 224.8 million acres planted on all crops, which is higher than average. It is 91.5 million acres more than anticipated.

Corn: The planted acreage report showed significant changes in the US since March. It shows more corn acreage are planted and fewer soybean and wheat acres. USDA pegs 2024 corn plantings at 91.5 million acres, which is more than a million acres above the agency’s March estimate, but more than 3 million acres below final 2023 tallies. The average estimate was for 90.353 million acres, with trade guesses ranging between 89 million and 91.3 million acres. As a result, corn futures stumbled 5% lower in the minutes immediately following the report’s release. With the change of administration in Mexico, GMO yellow corn products will continue to be allowed to be shipped to Mexico, the No. 1 export market for US corn producers.

Soybeans: A total of 86.1 million acres are planted in soybeans, which is higher than 2023 but less than estimated in March. Producers have 970 million bushels of soybeans in storage. It was up from March’s anticipated 962 million bushels in storage. There is an increase of 22 percent more in storage from 2023. Soybean plantings were closer to the mark but still reported-in moderately below analyst expectations.

Wheat: The report showed 47.2 million acres of wheat are planted, which is lower than 2023 and much lower than anticipated in the March forecast. When it comes to the Grain Stock report, farmers have 4.993 billion bushels in storage which was higher than anticipated and 22 percent more than in 2023.

The report showed 702 million bushels of wheat in storage, which was up 22% from 2023. Wheat acres are also expected to decline this season, with all-wheat plantings now projected at 47.2 million acres. That is a 5% decline from 2023-24. Analysts were expecting to see a slightly larger footprint after offering an average trade guess of 47.657 million acres.

Winter wheat plantings were also below the average trade guess in today’s report. Soybean acres are projected to move 3% higher from 2023 to 2024, with 86.1 million acres. That was a bit below the average trade guess of 86.753 million acres. It was also below USDA’s prior projection of 86.510 million acres that the agency made in late March. Of the total, USDA reports winter wheat plantings at 33.8 million acres, spring wheat plantings at 11.3 million acres and durum plantings at 2.17 million acres.

US wheat exports have declined for decades to the point that the US is considered a residual supplier to the global market, with Russia the top wheat exporter. Brazil has overtaken the US as the world’s largest soybean exporter, with China, the world’s largest soybean importer, indicating it favors doing business with Brazil. The US remains the world’s largest corn exporter by far, but Brazil also is making inroads in that sector, with recent record-high corn production and exports.

Because all South America is becoming more efficient at raising corn and soybeans, they are beginning to dominate global export markets -- 48% of the soybeans and 40% of corn originate from South America, up dramatically from just 10 years ago. US farmers will have to become better at dominating their own market because exports will be more competitive. Because of Mexico’s proximity to the US, it now boasts $6 billion in annual sales from US corn producers.

If you follow a five-year trend, grain-based feed ingredients including corn, wheat and soybean prices travel within a pricing range of one another. Their price also correlates to the price of oil. Controlling and reducing cost are always a key factor in a successful or unsuccessful year for good companies in the protein business. Ethanol production continues to get more efficient, maximizing the energy extracted from every bushel of corn. Ethanol is now the No. 1 consumer of corn, with animal feed ingredients close behind in second. Crude oil markets are back into the $84 per barrel range in July 2023, caused by OPEC moderating production during and a recent increase in consumption. President Biden’s release of millions of gallons of gasoline from the strategic reserve moderates this as well.

We have expressed long-term concerns about our farmers and their ability to continue supplying the feed ingredients we need on a cost-effective basis. Seventy percent of the farmland is changing hands in the next 15 years. This means the next generation of farmers need to take control and continue to produce the crops we need to feed our animals and supply ingredients for our baked goods.

Additionally, experts are genuinely concerned that we continue to lower our water tables and 10 years from now will have significant challenges with the water supply and Quality. Some areas of the U.S. are facing significant water stress such as Nebraska, Colorado, California, Delaware, Ohio, Virginia, North Carolina, Arkansas and the entire Southwest. As an industry we need to improve our stewardship of water use, returning it back into supply in the form of potable water. We also need to protect adjacent waterways.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!